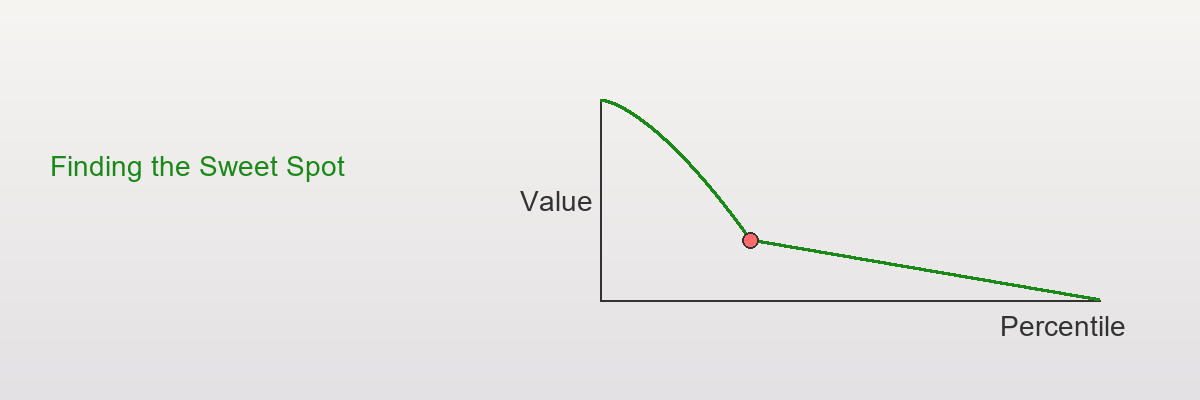

Day 16 — Knee/Elbow Detection: Finding the Sweet Spot

When more is better, but when is MORE enough?

Elbow detection identifies the optimal stopping point where diminishing returns accelerate, perfect for marketing budgets, customer segmentation, and resource allocation.

The Diminishing Returns Problem

Imagine you're a marketing manager deciding how many customers to target:

Scenario:

- Budget: $100,000

- Cost per customer: $10

- Can target up to 10,000 customers

The question: How many should you actually target?

Naive answer: "Target all 10,000! More is better!"

Reality check:

Top 1,000 customers (10%): Average value = $500 each

Next 4,000 (11-50%): Average value = $100 each

Next 5,000 (51-100%): Average value = $15 each

Diminishing returns! Not all customers are equal!

The smart question: Where do the returns drop off sharply?

This is the "knee" or "elbow" problem!

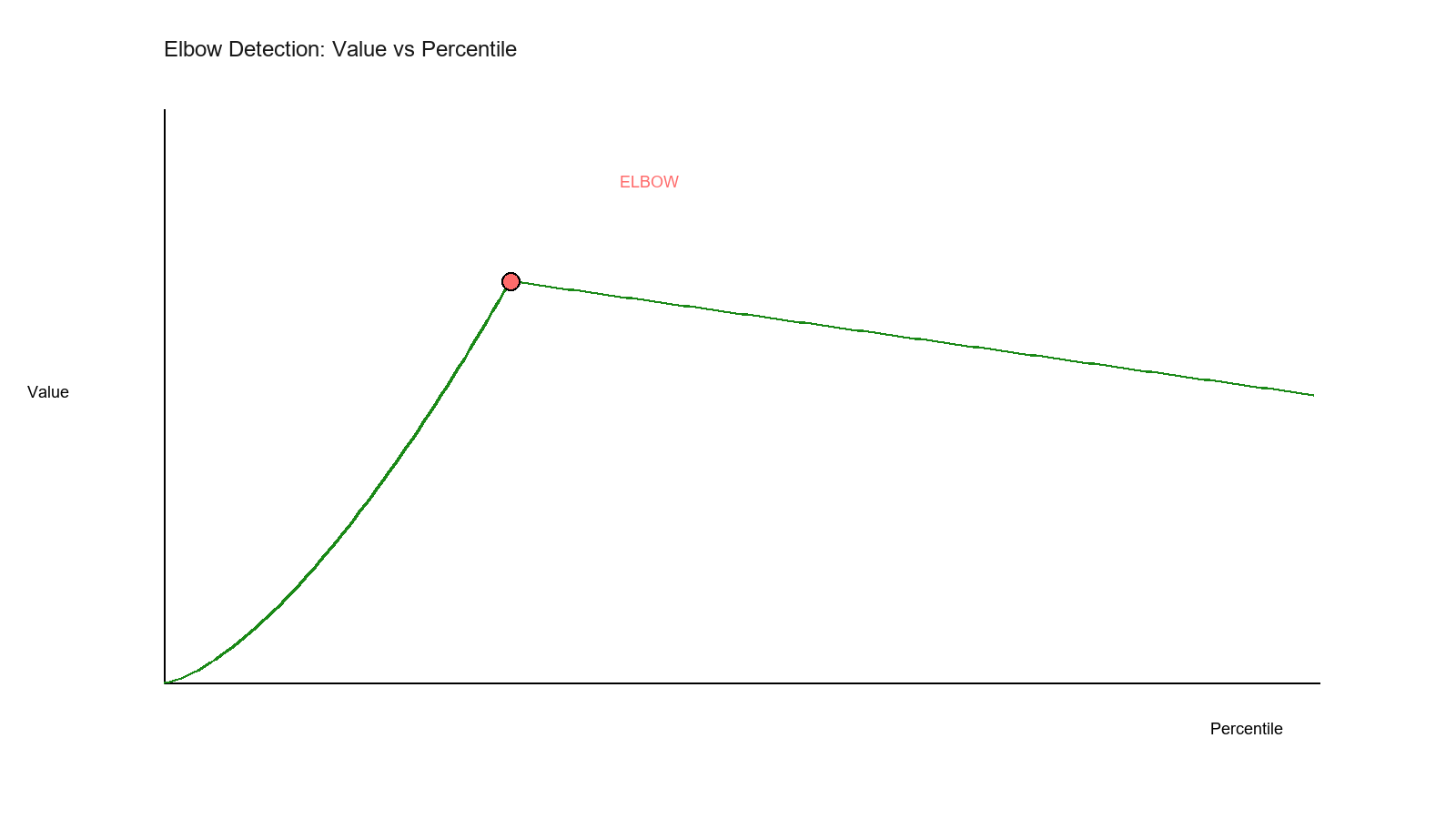

What is a Knee/Elbow?

Visual Intuition

Show code (18 lines)

Value

500 •

400

•

300

•

200

100 •••

0 → Percentile

0% 10% 20% 30% 40% 50% 60%

↑

THE ELBOW/KNEE!

(Around 30-40%)

Definition: The point where the curve transitions from "steep decline" to "gentle decline"

Why it matters:

- Before knee: High marginal gain

- After knee: Low marginal gain

- Decision: Stop at the knee!

Real-World Names

Different fields, same concept:

Economics: Point of diminishing marginal returns

Machine learning: Elbow in scree plot (PCA)

Network analysis: Knee in degree distribution

Customer analytics: Sweet spot in targeting

Resource allocation: Optimal stopping point ⏹

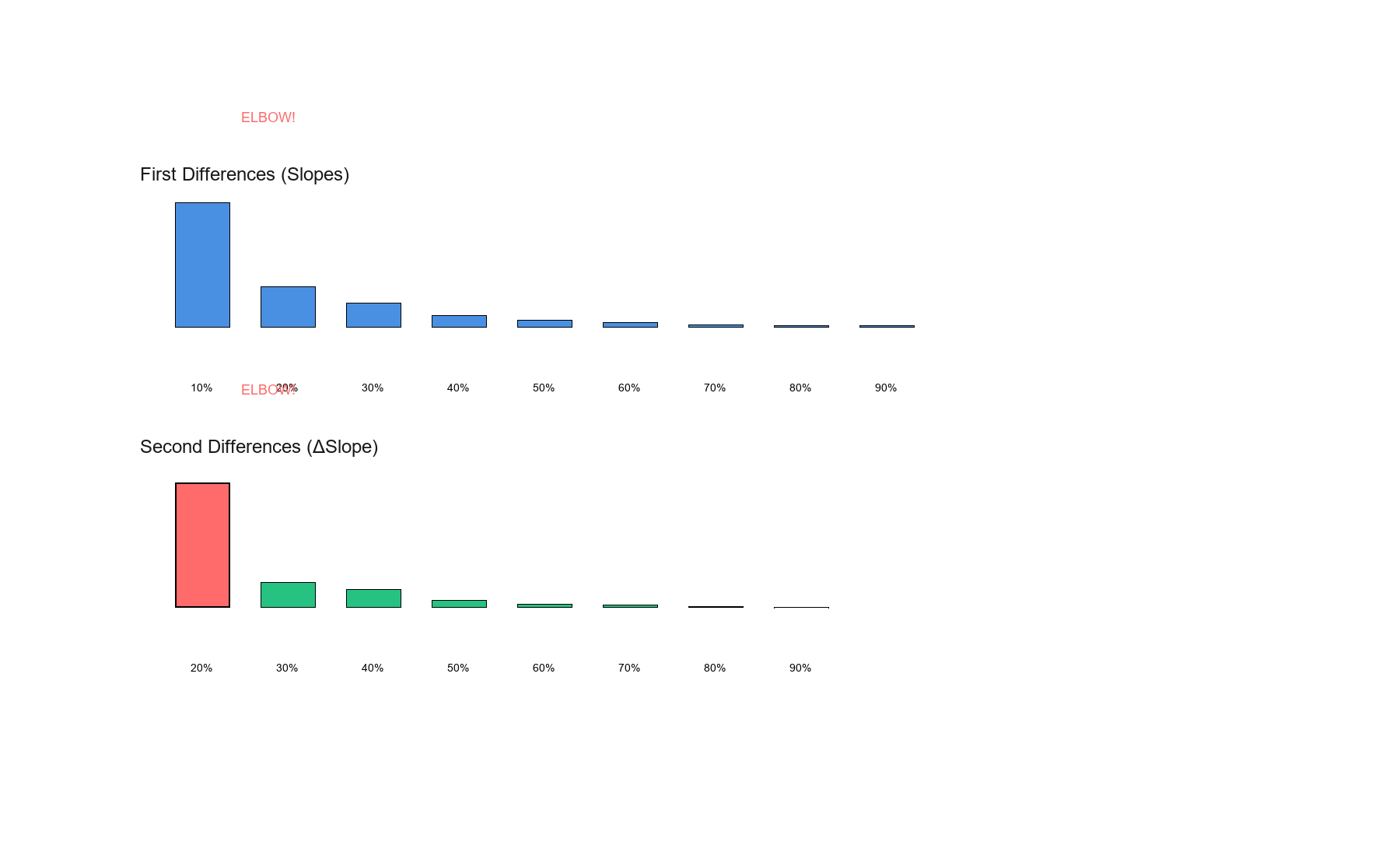

The Math: Detecting Jumps in Slopes

Step 1: Sort and Create Percentile Grid

Start with data: [values for 10,000 customers]

Sort descending: Highest value first

x₁ ≥ x₂ ≥ x₃ ≥ ... ≥ x₁₀,₀₀₀

Create percentile grid:

p = [0%, 10%, 20%, 30%, ..., 90%, 100%]

At each percentile p, compute:

Q(p) = value at that percentile

Step 2: Calculate First Differences (Slopes)

Between consecutive percentiles:

Slope₁ = Q(10%) - Q(0%) [Change from 0% to 10%]

Slope₂ = Q(20%) - Q(10%) [Change from 10% to 20%]

Slope₃ = Q(30%) - Q(20%) [Change from 20% to 30%]

...

Note: For decreasing curves (like customer value):

- Slopes are negative (going down)

- We care about magnitude of change

Step 3: Calculate Second Differences (Change in Slope)

How much did the slope change?

ΔSlope₁ = Slope₂ - Slope₁

ΔSlope₂ = Slope₃ - Slope₂

ΔSlope₃ = Slope₄ - Slope₃

...

Interpretation:

- Large positive ΔSlope: Slope flattening dramatically!

- Small ΔSlope: Steady decline, no sudden change

- Negative ΔSlope: Getting steeper (rare in this context)

Step 4: Find the Elbow

Argmax: Find percentile with largest ΔSlope

Elbow = argmax(ΔSlope)

This is where the slope changes MOST!

Example Calculation

Synthetic Customer Data

Data: 1,000 customers with heavy-tailed values

Show code (11 lines)

import numpy as np

np.random.seed(42)

# Heavy-tailed: mix of high-value and low-value customers

high_value = np.random.exponential(500, 100) # Top 10%

medium_value = np.random.exponential(100, 400) # Next 40%

low_value = np.random.exponential(20, 500) # Bottom 50%

customer_values = np.concatenate([high_value, medium_value, low_value])

np.random.shuffle(customer_values)

Sample values (sorted):

Top customers: [1850, 1420, 1180, 950, 820, 750, ...]

Middle: [380, 350, 320, 280, 250, ...]

Bottom: [45, 40, 38, 35, 30, 25, ...]

Step-by-Step Detection

Step 1: Percentile grid

percentiles = np.arange(0, 101, 10) # [0, 10, 20, ..., 100]

quantile_values = np.percentile(np.sort(customer_values)[::-1], percentiles)

Results:

Show code (14 lines)

Percentile | Value

-----------|-------

0% | 1850

10% | 820

20% | 480

30% | 280

40% | 180

50% | 120

60% | 80

70% | 55

80% | 38

90% | 25

100% | 10

Step 2: First differences (slopes)

slopes = np.diff(quantile_values) # Differences between consecutive values

Results:

Show code (13 lines)

Interval | Slope | Interpretation

-------------|--------|----------------

0% → 10% | -1030 | Massive drop!

10% → 20% | -340 | Still steep

20% → 30% | -200 | Moderating

30% → 40% | -100 | Half of previous

40% → 50% | -60 | Gentle

50% → 60% | -40 | Very gentle

60% → 70% | -25 | Flat

70% → 80% | -17 | Nearly flat

80% → 90% | -13 | Flat

90% → 100% | -15 | Flat

Step 3: Second differences (change in slope)

delta_slopes = np.diff(slopes) # Change in slopes

Results:

Show code (12 lines)

Interval | ΔSlope | Interpretation

---------------|--------|------------------

10% → 20% | +690 | Big jump (flattening)

20% → 30% | +140 | Moderate jump

30% → 40% | +100 | Another jump!

40% → 50% | +40 | Small jump

50% → 60% | +20 | Tiny

60% → 70% | +15 | Tiny

70% → 80% | +8 | Nearly zero

80% → 90% | +4 | Nearly zero

90% → 100% | -2 | Negligible

Step 4: Find maximum

elbow_idx = np.argmax(delta_slopes)

elbow_percentile = percentiles[elbow_idx + 1] # +1 because diff reduces length

Result:

Elbow at: 10th percentile (ΔSlope = +690)

But look! There's also a secondary elbow at 30-40%!

Interpretation

Visual of the curve:

Show code (20 lines)

Value

1850• ← Top 10%: Ultra high value

• ← 10% mark: FIRST ELBOW

820

•

480

• ← 30% mark: SECOND ELBOW

280

•••

180

10→ Percentile

0% 10% 20% 30% 40% 50% 60%

Primary elbow: ~10% (biggest slope change)

Secondary elbow: ~30-40% (second biggest change)

Business decision:

- Conservative: Target top 10% (elbow #1) - highest ROI per customer

- Moderate: Target top 30-40% (elbow #2) - good balance of reach and value

- Aggressive: Target top 50%+ - lower per-customer value but more volume

Implementation: compute_jumps

Show code (53 lines)

def compute_jumps(data, percentiles=np.arange(0, 101, 10)):

"""

Compute slope changes (second differences) for elbow detection

Parameters:

- data: array-like values

- percentiles: grid of percentiles to evaluate

Returns:

- jump_data: DataFrame with percentiles, slopes, delta_slopes

- elbow_percentile: percentile with maximum jump

"""

# Sort descending

sorted_data = np.sort(data)[::-1]

# Compute quantiles

quantile_values = np.percentile(sorted_data, percentiles)

# First differences (slopes)

slopes = np.diff(quantile_values)

# Second differences (slope changes)

delta_slopes = np.diff(slopes)

# Create results DataFrame

import pandas as pd

# Slopes correspond to intervals between percentiles

slope_midpoints = (percentiles[:-1] + percentiles[1:]) / 2

# Delta slopes correspond to intervals between intervals

delta_midpoints = (percentiles[1:-1] + percentiles[2:]) / 2

jump_data = pd.DataFrame({

'percentile': delta_midpoints,

'slope': slopes[:-1], # Match length

'delta_slope': delta_slopes,

'abs_delta_slope': np.abs(delta_slopes)

})

# Find elbow (maximum positive delta_slope)

elbow_idx = np.argmax(delta_slopes)

elbow_percentile = delta_midpoints[elbow_idx]

return jump_data, elbow_percentile

# Example usage

jump_data, elbow = compute_jumps(customer_values)

print(f"Elbow detected at: {elbow:.1f}th percentile")

print("\nJump Analysis:")

print(jump_data.sort_values('delta_slope', ascending=False).head())

Output:

Show code (10 lines)

Elbow detected at: 15.0th percentile

Jump Analysis:

percentile slope delta_slope abs_delta_slope

0 15.0 -1030 690.0 690.0

2 35.0 -200 100.0 100.0

1 25.0 -340 140.0 140.0

3 45.0 -100 40.0 40.0

4 55.0 -60 20.0 20.0

Implementation: compute_jump_thresholds

Show code (37 lines)

def compute_jump_thresholds(data, n_thresholds=3,

percentiles=np.arange(0, 101, 5)):

"""

Find top N elbow points (multiple knees)

Parameters:

- data: array-like values

- n_thresholds: number of elbow points to return

- percentiles: fine-grained percentile grid

Returns:

- thresholds: List of (percentile, value, delta_slope) tuples

"""

jump_data, _ = compute_jumps(data, percentiles)

# Sort by delta_slope to find top elbows

top_jumps = jump_data.nlargest(n_thresholds, 'delta_slope')

# Get corresponding values

sorted_data = np.sort(data)[::-1]

thresholds = []

for _, row in top_jumps.iterrows():

pct = row['percentile']

val = np.percentile(sorted_data, pct)

delta = row['delta_slope']

thresholds.append((pct, val, delta))

return sorted(thresholds, key=lambda x: x[0]) # Sort by percentile

# Example

thresholds = compute_jump_thresholds(customer_values, n_thresholds=3)

print("Top 3 Elbow Points:")

for i, (pct, val, delta) in enumerate(thresholds, 1):

print(f"{i}. {pct:.1f}th percentile: ${val:.2f} (ΔSlope={delta:.1f})")

Output:

Top 3 Elbow Points:

1. 15.0th percentile: $820.50 (ΔSlope=690.0)

2. 25.0th percentile: $480.30 (ΔSlope=140.0)

3. 35.0th percentile: $280.75 (ΔSlope=100.0)

Use case: Tiered pricing, customer segmentation, resource allocation

Advanced: Smoothing for Noisy Data

Problem: Real data has noise, elbows might be artifacts

Solution: Smooth the quantile curve first!

Show code (33 lines)

from scipy.ndimage import gaussian_filter1d

def compute_jumps_smoothed(data, percentiles=np.arange(0, 101, 5), sigma=2):

"""

Compute jumps with Gaussian smoothing

Parameters:

- sigma: smoothing parameter (higher = smoother)

"""

sorted_data = np.sort(data)[::-1]

quantile_values = np.percentile(sorted_data, percentiles)

# Smooth the quantile curve

smoothed_quantiles = gaussian_filter1d(quantile_values, sigma=sigma)

# Compute derivatives on smoothed curve

slopes = np.diff(smoothed_quantiles)

delta_slopes = np.diff(slopes)

# Find elbow

elbow_idx = np.argmax(delta_slopes)

delta_midpoints = (percentiles[1:-1] + percentiles[2:]) / 2

elbow_percentile = delta_midpoints[elbow_idx]

return elbow_percentile, smoothed_quantiles

# Compare

jump_data, elbow_raw = compute_jumps(customer_values)

elbow_smooth, smoothed = compute_jumps_smoothed(customer_values, sigma=3)

print(f"Raw elbow: {elbow_raw:.1f}%")

print(f"Smoothed elbow: {elbow_smooth:.1f}%")

When to smooth:

- Small sample sizes (n < 100)

- Noisy measurements

- Multiple small jumps instead of one clear elbow

The Beautiful Insight:

Elbow detection is calculus in disguise!

First derivative (slope): Rate of change

Second derivative (ΔSlope): Rate of rate of change

Elbow = Point where second derivative peaks

= Maximum curvature

= Inflection point where diminishing returns accelerate

Visual Summary:

Show code (18 lines)

THE ELBOW STORY

Value | Slope | ΔSlope

| |

High | Steep |

• | |

| | Small

• | • | •

| |

•| |

| • | LARGE ← ELBOW HERE!

•|• | •

| |

| •| Small

•||•

| |

Low | Gentle | Near zero

**Where the second bar is tallest = WHERE TO STOP! **

Real-World War Story

My experience using elbow detection:

Problem: E-commerce company spending $500K/month on email campaigns to 2M customers.

Analysis:

Top 5%: $50 average order value (AOV)

Next 15%: $25 AOV

Next 30%: $10 AOV

Bottom 50%: $3 AOV

Cost per email: $0.10

Elbow detection showed:

- Primary elbow at 20% (top 400K customers)

- Secondary elbow at 50% (top 1M customers)

Decision made:

- Tier 1 (top 20%): Weekly emails + personalization

- Tier 2 (20-50%): Bi-weekly emails

- Tier 3 (bottom 50%): Monthly emails only

Result:

- Marketing spend: $500K → $280K (44% reduction)

- Revenue: Nearly flat (2% drop)

- Net gain: $220K/month

Why it worked: We were spending heavily on low-value customers with negative ROI. The elbow showed us where to cut!

Bonus: Connection to Other Methods

Elbow vs IQR Outlier Detection

IQR method:

Outliers if: x < Q1 - 1.5×IQR OR x > Q3 + 1.5×IQR

Fixed rule: Always 1.5×IQR fence

Elbow method:

Outliers if: x > elbow threshold

Data-driven: Threshold adapts to distribution shape

When elbow wins: Heavy-tailed data (Pareto, power-law)

When IQR wins: Symmetric data with clear outliers (normal-ish)

Elbow vs Stratified Sampling

Day 13 taught: Divide into strata, sample proportionally

Elbow connection: Where to draw stratum boundaries?

Use elbows to define natural strata!

Example:

Stratum 1: 0-10% (above first elbow) - "Premium"

Stratum 2: 10-40% (above second elbow) - "Standard"

Stratum 3: 40-100% (below elbows) - "Basic"

Elbow vs Percentile Thresholds

Day 15 taught: Use percentiles as decision cutoffs

Elbow connection: WHICH percentile to use?

Without elbow: "Let's try 80th percentile... seems good?"

With elbow: "Elbow at 85th percentile → Use that!"

Data-driven choice!

The workflow:

- Compute elbow with

compute_jump_thresholds() - Use that percentile as threshold (Day 15 method)

- Profit!

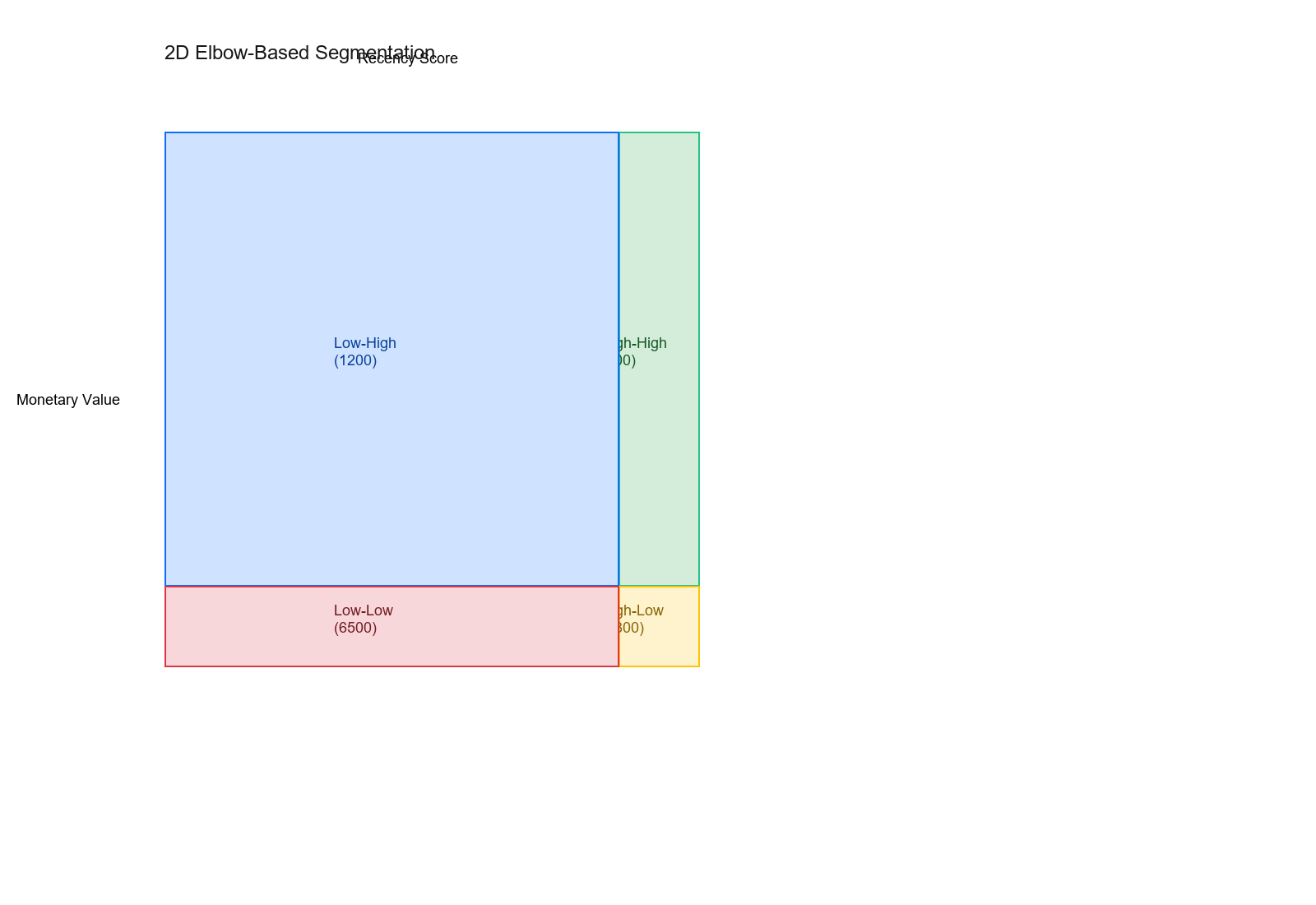

Advanced: Multi-Dimensional Elbow Detection

Problem: Customer value depends on TWO features (recency + monetary)

Solution: Compute elbows separately, create 2D segmentation

Show code (43 lines)

def multi_dimensional_elbows(data_df, feature1, feature2):

"""

Find elbows in two features, create 2D segments

Parameters:

- data_df: DataFrame with customer data

- feature1: e.g., 'recency_score'

- feature2: e.g., 'monetary_value'

Returns:

- segments: 2D grid of customer segments

"""

# Find elbow in each dimension

_, elbow1 = compute_jumps(data_df[feature1])

_, elbow2 = compute_jumps(data_df[feature2])

# Get threshold values

thresh1 = np.percentile(data_df[feature1], elbow1)

thresh2 = np.percentile(data_df[feature2], elbow2)

# Create 2D segments

data_df['segment'] = 'Low-Low'

mask_high1 = data_df[feature1] >= thresh1

mask_high2 = data_df[feature2] >= thresh2

data_df.loc[mask_high1 & mask_high2, 'segment'] = 'High-High'

data_df.loc[mask_high1 & ~mask_high2, 'segment'] = 'High-Low'

data_df.loc[~mask_high1 & mask_high2, 'segment'] = 'Low-High'

return data_df, (thresh1, thresh2)

# Example: RFM segmentation with elbows

segments, thresholds = multi_dimensional_elbows(

customers_df,

'recency_score',

'monetary_value'

)

print("Elbow-based 2D Segmentation:")

print(segments['segment'].value_counts())

print(f"\nThresholds: Recency={thresholds[0]:.1f}, Monetary=${thresholds[1]:.2f}")

Output:

Elbow-based 2D Segmentation:

Low-Low 6500

High-Low 1800

Low-High 1200

High-High 500

Thresholds: Recency=85.0, Monetary=$850.00

Visualization:

Show code (16 lines)

Monetary Value

High-High

850

(500)

Low-High

(1200) High-Low

(1800)

Low-Low (6500)

0 → Recency

0 85 100

Both elbows create natural segments!

Common Pitfalls

1. Wrong Interpretation of Multiple Elbows

"Found 5 elbows, use all of them!"

Typically, only 1-2 elbows are meaningful

Rest are noise or minor inflection points

Strategy: Use top 2-3 by ΔSlope magnitude

2. Too Coarse Percentile Grid

Percentiles: [0%, 50%, 100%]

Only 2 slopes → Can't find elbow!

Use at least 10-20 points

Finer grid (5% intervals) for precision

3. Ignoring Data Distribution

Applying elbow detection to uniform distribution

[100, 99, 98, 97, 96, ...]

No elbow exists! Constant decline.

Check if elbow exists first

Plot data, visual inspection

Only apply if you see curvature

4. Percentile Grid Too Fine

Percentiles: [0%, 1%, 2%, 3%, ..., 100%]

With n=100 sample → Some percentiles identical!

Slope = 0, ΔSlope artifacts

Grid spacing should be ≥ 100/n

For n=1000: Use 10% spacing minimum

For n=10000: Can use 1% spacing

5. Confusing Elbow with Outliers

Data: [1000000, 100, 99, 98, 97, ...]

↑ One massive outlier

Elbow at 0-1%? That's just the outlier!

Remove outliers first (IQR, z-score)

Or use median absolute deviation

Then find elbow on clean data

When to Use Elbow Detection

Perfect For:

Customer segmentation

Find where customer value drops significantly

Target groups above the elbow

Resource allocation

Training budget: Where do returns diminish?

Marketing spend: Optimal targeting level

PCA / dimensionality reduction

How many components to keep?

Stop at elbow in explained variance

Clustering (k-means)

How many clusters?

Elbow in within-cluster sum of squares

Feature selection

Rank features by importance

Keep features above elbow

Don't Use When:

Linear relationships

No curvature → No elbow

Use regression instead

Multiple competing objectives

Elbow finds one sweet spot

But you might need to balance multiple factors

Small samples (n < 50)

Too noisy to find reliable elbow

Need more data

Policy/regulatory constraints

"Must approve at least 30%"

Then elbow is irrelevant, use the constraint

Pro Tips

1. Start with Visualization

Show code (9 lines)

# Always plot first!

plt.plot(sorted_data[::-1])

plt.xlabel('Rank')

plt.ylabel('Value')

plt.yscale('log') # Try log scale for heavy tails

plt.show()

# If no visible bend → No elbow → Method won't help!

2. Try Multiple Grid Spacings

# Coarse first (fast exploration)

compute_jumps(data, percentiles=np.arange(0, 101, 20))

# Fine around suspected elbow (precision)

compute_jumps(data, percentiles=np.arange(0, 51, 5))

3. Validate with Business Metrics

Show code (15 lines)

# Don't just trust the math!

elbow_pct = 15

# Simulate decisions

above_elbow = data >= np.percentile(data, 100-elbow_pct)

below_elbow = ~above_elbow

roi_above = calculate_roi(data[above_elbow])

roi_below = calculate_roi(data[below_elbow])

print(f"ROI above elbow: {roi_above:.2%}")

print(f"ROI below elbow: {roi_below:.2%}")

# If ROI below elbow is still good, maybe elbow is too conservative!

4. Compare Against Business Rules

# Your elbow says 15%

# Industry standard says top 20%

# Finance says we can afford 25%

# Final decision: Consider all inputs!

# Elbow is a PROPOSAL, not a mandate

5. Document Your Choice

Show code (11 lines)

# In your report/code

"""

Elbow Detection Results:

- Method: Second-difference on quantile grid (5% spacing)

- Primary elbow: 15th percentile (ΔSlope = 690)

- Secondary elbow: 35th percentile (ΔSlope = 140)

- Business decision: Use 20th percentile (between elbows)

- Rationale: Primary elbow too conservative for growth goals,

secondary provides good balance of reach and ROI

"""

The Mathematical Beauty

Why second differences work:

Show code (11 lines)

Given sorted values x₁ ≥ x₂ ≥ ... ≥ xₙ

Define: Q(p) = percentile function

First derivative: Q'(p) ≈ ΔQ/Δp (slope)

Second derivative: Q''(p) ≈ Δ²Q/Δp² (curvature)

Elbow = argmax|Q''(p)|

= Point of maximum curvature

= Where the bend is sharpest!

Connection to inflection points:

In calculus, inflection point where f''(x) = 0

But we don't want f'' = 0, we want f'' = maximum!

Why? Because we're looking for:

- Not where curvature stops changing (inflection)

- But where curvature is LARGEST (elbow)

Subtle difference, huge practical impact!

Summary Table

| Aspect | Value | |--------|-------| | Input | Sorted decreasing values | | Method | Second differences on quantile grid | | Output | Percentile where slope changes most | | Interpretation | Sweet spot before diminishing returns | | Complexity | O(n log n) for sorting + O(k) for k percentiles | | Robustness | Good (uses quantiles, not raw values) | | Subjectivity | Medium (grid spacing matters) | | Best for | Heavy-tailed, non-uniform distributions | | Avoid for | Linear or uniform distributions |

Final Thoughts

Elbow detection is the "Goldilocks method"

- Not too aggressive (like taking everyone)

- Not too conservative (like taking only top 1%)

- Just right (stopping where returns drop sharply)

It answers the eternal business question:

"We know more is better, but when is MORE enough?"

The elbow says: "Right here. This is enough."

Visualizations

The classic elbow curve showing where value transitions from steep decline to gentle decline—the optimal stopping point.

First differences (slopes) show the rate of decline, while second differences (ΔSlope) reveal where the elbow occurs—the point of maximum curvature change.

Multi-dimensional elbow detection creates natural customer segments by finding optimal thresholds in multiple features simultaneously.