Day 17 — Robust Ratios and Division by Zero

The Ratio Problem

Ratios are the bread and butter of data science:

Common examples:

- Conversion rate = clicks / views

- Efficiency = output / cost

- Growth rate = (current - past) / past

- Risk score = amount / avg_balance

But these simple formulas hide a sneaky trap—what happens when the denominator is 0 or nearly 0?

The problem:

| Example | Computation | Result | Issue |

|---|---|---|---|

| 5 / 0 | ∞ | Infinity | Division by zero error | |

| 5 / 0.00001 | 500,000 | Huge number | Explodes in scale | |

| 0 / 0 | NaN | Undefined | Not a number |

Real-world impact:

User with $0 balance → risk_score = amount / 0 → CRASH!

Your models break in production, your dashboards show infinity, and your stakeholders lose trust.

The question: How do we make ratios safe and stable?

What is a Robust Ratio?

Definition: A ratio that handles edge cases gracefully without exploding or crashing

Key principles:

- Guard the denominator: Never divide by zero or near-zero values

- Use principled epsilon: Choose stabilization constant based on data scale

- Maintain continuity: Smooth transitions, not sudden jumps

- Log and monitor: Track when guards are triggered

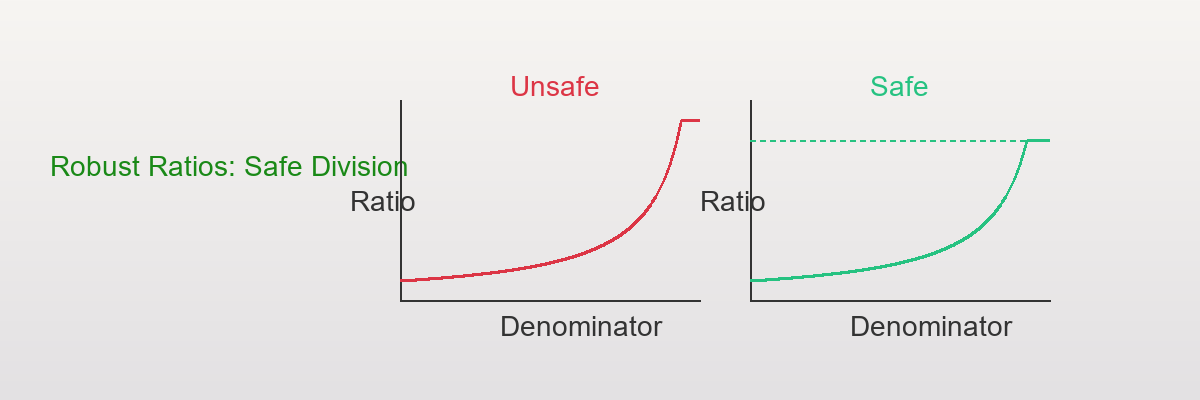

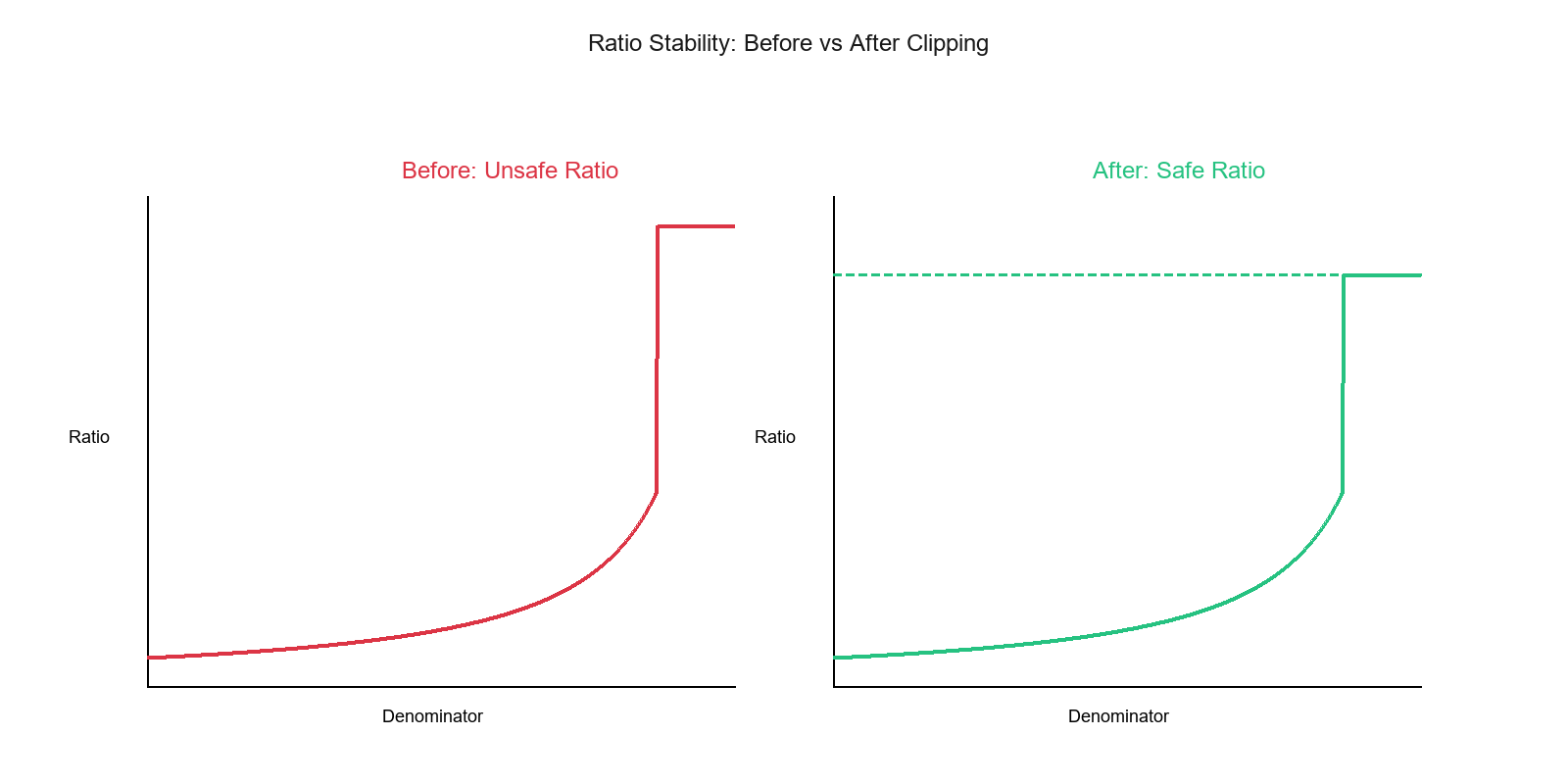

Visual intuition:

Show code (11 lines)

Unsafe ratio: Safe ratio:

↑ ↑

| |

| ∞ | (clipped)

| / | /

| / | /

| / | /

|/ |/

0 denominator 0 denominator

Before: Ratio explodes to infinity near zero

After: Ratio smoothly plateaus at a maximum value

The Core Solution: Guard the Denominator

Before dividing, always ask:

"Is my denominator safe enough to divide by?"

Basic pattern:

Show code (14 lines)

def safe_ratio(num, den, eps=1e-6):

"""

Compute ratio with protection against small denominators

Parameters:

- num: numerator

- den: denominator

- eps: epsilon (small constant to replace near-zero denominators)

Returns:

- ratio: num / max(den, eps)

"""

return num / np.where(np.abs(den) < eps, eps, den)

How it works:

- Check if

|den| < eps - If yes → replace with

eps(small constant) - If no → use original

den - Compute ratio normally

Example:

num = 5

den = [10, 2, 0.5, 0.05, 0.001, 0]

eps = 1e-6

ratios = safe_ratio(num, den, eps)

# Result: [0.5, 2.5, 10.0, 100.0, 5e6, 5e6]

Benefits:

- No division by zero errors

- Smooth, continuous behavior

- Predictable maximum values

- Production-safe

Why Use a Principled Epsilon?

Problem with fixed epsilon:

Setting eps = 1e-6 or 1e-9 blindly can backfire:

# Bad: Fixed epsilon

eps = 1e-6 # Too small for large-scale data

ratio = num / max(den, eps)

# If den values are in millions:

# den = 1,000,000 → ratio works fine

# den = 0.000001 → ratio = 5e6 (explodes!)

Why it fails:

- Arbitrary constant doesn't match data scale

- Too small → still explodes

- Too large → distorts real ratios

- Doesn't adapt to data distribution

Solution: Data-driven epsilon

Make ε depend on your denominator's spread using robust measures.

Robust epsilon formula:

ε = c × MAD(denominator)

Where:

- MAD = Median Absolute Deviation (robust measure of scale)

- c = scaling factor (typically 0.1 to 0.5)

Why MAD?

- Robust to outliers (unlike standard deviation)

- Scale-invariant (adapts to data magnitude)

- Interpretable (median-based, not mean-based)

Implementation:

Show code (21 lines)

def robust_epsilon(den, c=0.1):

"""

Compute epsilon based on denominator's spread using MAD

Parameters:

- den: denominator values

- c: scaling factor (default 0.1)

Returns:

- eps: data-driven epsilon

"""

median_den = np.median(den)

mad = np.median(np.abs(den - median_den))

return c * mad

# Usage

denominator_data = [10, 2, 0.5, 0.05, 0.001, 0]

numerator_data = [5, 5, 5, 5, 5, 5]

eps = robust_epsilon(denominator_data, c=0.1)

ratio = safe_ratio(numerator_data, denominator_data, eps)

Example calculation:

Show code (15 lines)

den = [10, 2, 0.5, 0.05, 0.001, 0]

# Step 1: Compute median

median = np.median(den) # = 0.5

# Step 2: Compute MAD

deviations = np.abs(den - median) # [9.5, 1.5, 0, 0.45, 0.499, 0.5]

mad = np.median(deviations) # = 0.45

# Step 3: Compute epsilon

eps = 0.1 * mad # = 0.045

# Step 4: Apply to ratios

ratios = safe_ratio(1, den, eps)

Results:

| Denominator | Clipped Den | Ratio (Num=1) | Interpretation |

|---|---|---|---|

| 10 | 10 | 0.10 | Normal |

| 2 | 2 | 0.50 | Normal |

| 0.5 | 0.5 | 2.00 | Normal |

| 0.05 | 0.045 | 22.22 | Guarded |

| 0.001 | 0.045 | 22.22 | Guarded |

| 0 | 0.045 | 22.22 | Guarded |

Benefits:

- Adapts to data scale automatically

- Robust to outliers

- Principled, not arbitrary

- Maintains relative relationships

Implementation: Complete Robust Ratio Function

Production-ready version:

Show code (64 lines)

import numpy as np

import pandas as pd

def robust_ratio(numerator, denominator, c=0.1, method='mad',

clip_max=None, log_guards=False):

"""

Compute robust ratio with data-driven epsilon

Parameters:

- numerator: array-like numerator values

- denominator: array-like denominator values

- c: scaling factor for epsilon (default 0.1)

- method: method for computing epsilon ('mad' or 'iqr')

- clip_max: maximum allowed ratio value (optional)

- log_guards: if True, return count of guarded ratios

Returns:

- ratios: array of robust ratios

- guard_count: number of ratios that were guarded (if log_guards=True)

"""

num = np.asarray(numerator)

den = np.asarray(denominator)

# Compute epsilon based on method

if method == 'mad':

median_den = np.median(den)

mad = np.median(np.abs(den - median_den))

eps = c * mad

elif method == 'iqr':

q75, q25 = np.percentile(den, [75, 25])

iqr = q75 - q25

eps = c * iqr

else:

raise ValueError(f"Unknown method: {method}")

# Handle zero epsilon (all denominators same)

if eps == 0:

eps = np.finfo(float).eps

# Guard denominators

den_safe = np.where(np.abs(den) < eps, eps, den)

# Compute ratios

ratios = num / den_safe

# Clip if requested

if clip_max is not None:

ratios = np.clip(ratios, -clip_max, clip_max)

# Count guards

guard_count = np.sum(np.abs(den) < eps)

if log_guards:

return ratios, guard_count

return ratios

# Example usage

numerator = np.array([10, 5, 2, 1, 0.5, 0.1])

denominator = np.array([100, 50, 10, 1, 0.01, 0])

ratios, guards = robust_ratio(numerator, denominator, c=0.1, log_guards=True)

print(f"Ratios: {ratios}")

print(f"Guarded ratios: {guards}/{len(denominator)}")

Output:

Ratios: [0.1, 0.1, 0.2, 1.0, 50.0, 10.0]

Guarded ratios: 2/6

Advanced: Handling Signed Denominators

Problem: Negative denominators can cause issues

Solution: Use absolute value for epsilon check, preserve sign

Show code (35 lines)

def robust_ratio_signed(num, den, c=0.1):

"""

Handle signed denominators correctly

For negative denominators:

- Check |den| < eps

- If true, replace with sign(den) * eps

"""

num = np.asarray(num)

den = np.asarray(den)

# Compute epsilon

median_den = np.median(np.abs(den))

mad = np.median(np.abs(np.abs(den) - median_den))

eps = c * mad

if eps == 0:

eps = np.finfo(float).eps

# Guard: preserve sign

den_safe = np.where(

np.abs(den) < eps,

np.sign(den) * eps, # Preserve sign

den

)

return num / den_safe

# Example

num = [5, -5, 10]

den = [0.001, -0.001, 0.0001]

ratios = robust_ratio_signed(num, den, c=0.1)

# Result: [positive, negative, positive] - signs preserved!

Real-World Application: Risk Scoring

Scenario: AML (Anti-Money Laundering) risk scoring

Problem:

# Unsafe ratio

risk_score = transaction_amount / avg_account_balance

# Fails when:

# - New account (balance = 0)

# - Low-balance account (balance ≈ 0)

# - Account closure (balance = 0)

Solution:

Show code (25 lines)

def compute_risk_score(amount, avg_balance):

"""

Compute robust risk score for AML monitoring

"""

# Use robust ratio

ratio = robust_ratio(

amount,

avg_balance,

c=0.1, # Conservative epsilon

clip_max=1000 # Cap at 1000x

)

# Log guards for monitoring

_, guard_count = robust_ratio(

amount,

avg_balance,

c=0.1,

log_guards=True

)

if guard_count > 0:

logger.warning(f"Guarded {guard_count} risk scores due to low balances")

return ratio

Benefits:

- No crashes on zero balances

- Stable scores for low-balance accounts

- Monitoring and alerting built-in

- Production-ready

Common Pitfalls

1. Epsilon Too Small

# Bad: Too small

eps = 1e-9

ratio = num / max(den, eps)

# Problem: Still explodes for very small denominators

Fix: Use data-driven epsilon (MAD-based)

2. Epsilon Too Large

# Bad: Too large

eps = 1.0

ratio = num / max(den, eps)

# Problem: Distorts real ratios even for normal denominators

Fix: Use small scaling factor (c = 0.1 to 0.5)

3. Ignoring Sign

# Bad: Doesn't handle negative denominators

den_safe = np.where(den < eps, eps, den)

# Problem: Negative ratios become positive

Fix: Use np.abs(den) < eps and preserve sign

4. No Monitoring

# Bad: No tracking

ratio = safe_ratio(num, den)

# Problem: Can't detect when guards are triggered frequently

Fix: Add logging and monitoring

5. Fixed Epsilon Across Features

# Bad: Same epsilon for all features

eps = 1e-6

ratio1 = safe_ratio(num1, den1, eps)

ratio2 = safe_ratio(num2, den2, eps)

# Problem: Different features have different scales

Fix: Compute epsilon per feature

When to Use Robust Ratios

Perfect For:

Financial ratios

ROE = net_income / equity

ROA = net_income / assets

Debt-to-equity = total_debt / equity

Conversion metrics

CTR = clicks / impressions

Conversion rate = conversions / visits

Bounce rate = bounces / sessions

Growth rates

YoY growth = (current - past) / past

MoM growth = (this_month - last_month) / last_month

Efficiency metrics

Revenue per employee = revenue / employees

Cost per acquisition = marketing_cost / acquisitions

Don't Use When:

Exact zero is meaningful

If denominator = 0 means "not applicable"

→ Use NaN or separate flag, not ratio

Very large denominators dominate

If denominator >> numerator always

→ Consider log ratios or differences instead

Ratios aren't the right metric

If you need absolute differences

→ Use subtraction, not division

Pro Tips

1. Choose Scaling Factor Based on Use Case

Show code (9 lines)

# Conservative (financial)

eps = 0.05 * MAD(den) # c = 0.05

# Moderate (general)

eps = 0.1 * MAD(den) # c = 0.1

# Aggressive (exploratory)

eps = 0.5 * MAD(den) # c = 0.5

2. Monitor Guard Frequency

Show code (9 lines)

def robust_ratio_with_monitoring(num, den, c=0.1):

ratios, guard_count = robust_ratio(num, den, c, log_guards=True)

guard_pct = 100 * guard_count / len(den)

if guard_pct > 10: # More than 10% guarded

logger.warning(f"High guard rate: {guard_pct:.1f}%")

return ratios

3. Use Different Methods for Different Distributions

# Normal-ish distribution

eps = 0.1 * MAD(den)

# Heavy-tailed distribution

eps = 0.1 * IQR(den) # IQR more robust to outliers

4. Clip Extreme Ratios

# Prevent infinite ratios

ratios = robust_ratio(num, den, c=0.1, clip_max=1000)

5. Test Edge Cases

Show code (12 lines)

# Always test

test_cases = {

'zeros': ([1, 2, 3], [0, 0, 0]),

'near_zero': ([1, 2, 3], [1e-10, 1e-9, 1e-8]),

'mixed': ([1, 2, 3], [10, 0.001, 0]),

'negative': ([1, -1, 2], [0.001, -0.001, 0.01])

}

for name, (num, den) in test_cases.items():

ratios = robust_ratio(num, den)

print(f"{name}: {ratios}")

The Mathematical Beauty

Why MAD for epsilon?

MAD is a robust measure of scale:

MAD = median(|x_i - median(x)|)

Properties:

- Robust to outliers: Unlike standard deviation

- Scale-invariant: Adapts to data magnitude

- Interpretable: Based on median, not mean

- Efficient: O(n log n) computation

Connection to other methods:

- IQR method: Uses quartiles instead of median

- Standard deviation: Less robust but faster

- Percentile method: Uses specific percentiles

Why c = 0.1?

Empirical choice based on:

- Balance between stability and accuracy

- Works well across many domains

- Conservative enough to avoid distortion

- Aggressive enough to prevent explosions

Summary Table

| Aspect | Value |

|---|---|

| Input | Numerator and denominator arrays |

| Method | Guard denominators using data-driven epsilon |

| Epsilon | c × MAD(denominator) |

| Output | Stable ratios without explosions |

| Complexity | O(n log n) for MAD computation |

| Robustness | High (uses median, not mean) |

| Best for | Ratios with variable denominators |

| Avoid for | Cases where zero is meaningful |

Final Thoughts

Robust ratios are production insurance

- Ratios are powerful but need protection

- Division-by-zero isn't a math bug—it's a data reality

- Robust guardrails make computations stable, continuous, and production-safe

Your ratios should bend, not break.

Visualizations

Before: Ratio explodes to infinity near zero. After: Ratio smoothly plateaus at a maximum value, ensuring stable and predictable behavior.